What is Supply?

- The amount of goods or services that producers are willing and able to offer at any price level during a specific time period, ceteris paribus.

- The quantity of a good suppliers are able to supply at any price level is the effective supply.

The Law of Supply

- The main principle of supply is the opposite of the principal of demand.

- In demand the lower the price, the more people want something, whereas in supply the higher the price, the more people want to supply something.

- "As the price of a product rises, the quantity supplied of the product will usually increase ceteris paribus."

- From this law it can be inferred that the quantity supplied is directly proportional to price.

- Higher prices lead to an increase in supply, as there is more opportunity for profit.

- Marginal cost (the additional cost of producing more units) can be covered more easily.

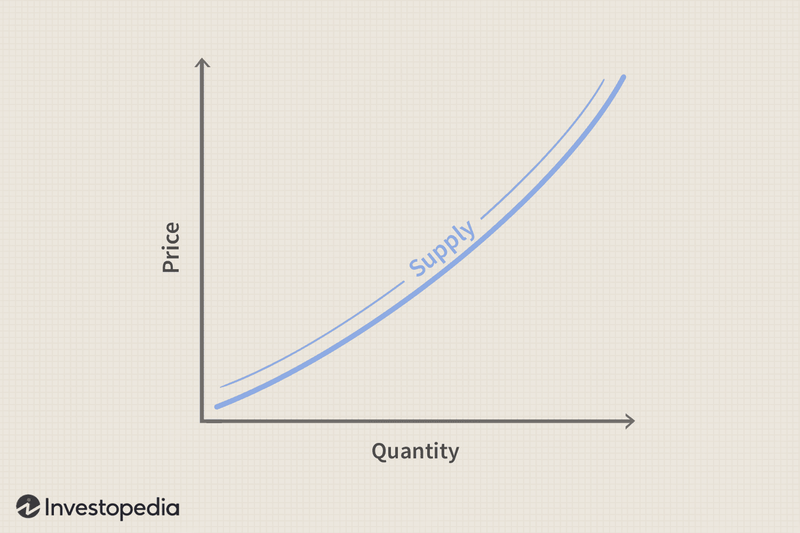

Graphing Supply

- Supply curves on a graph usually go upwards, the opposite to demand curves.

- This is because supply increases with price.

- If the price changes, the point on the supply curve will change, but if a non-price determinant of supply changes instead, the entire curve will shift to the right or left.

(The supply curve is generally drawn as a straight line for simplicity)

The Non-Price Determinants of Supply

Cost of Production

- The most significant non-price determinant of supply. If a product costs too much to produce, then suppliers cannot reasonably cover their costs or make profit, and thus will not supply the product.

- Many other non-price determinants affect this determinant in one way or the other.

- The costs of factors of production (management, labor, capital, land)

- For example if the cost of materials used in producing a product increases, there is a decrease in supply and the supply curve shifts left.

- The price needs to increase to meet the same supply as before.

- If the cost for production goes down, then the curve shifts to the right.

The State of Technology

- Improvements in technology will increase productivity, allowing for more supply with the same resources.

- While this generally results in a shift in the supply curve to the right, leading to decreased market price, in some situations firms might opt in to make more profit instead.

Government Intervention

- Indirect taxes and subsidies applied to products, as well as minimum and maximum price levels.

- Taxes and minimum price levels aim to increase price and reduce supply, resulting in a decrease in quantity demanded.

- Subsidies and maximum price levels can be used to increase the quantity demanded, either by increasing supply, thus reducing the market price, or by causing a direct reduction in the market price.

Examples

- If a government wants increased production of a good, they can subsidize it instead.

- Subsidization is the government funding of the production of a good, making it cheaper to produce, and increasing supply.

- Subsidization is also used to reduce the price level of a product, which can be beneficial in some sectors such as healthcare and education.

- The supply curve will shift to the right.

Future Expectations

- Producers can withhold or push products based on expectations for future prices.

- The effect that expectations can have on production varies.

- Expectations and confidence matter.

Future Price

- If firms expect prices of the products they sell to increase in the near future they might withhold part of their current production from the market (by not offering it for sale and storing it, also called hoarding) in the hope of being able to sell more at a higher price in the future.

Future Economy

- If producers expect the economy to do well, they will expect that people will have more money to spend and that the consumption of goods and services will increase.

Examples

- A firm could try to get rid of a product if the Government is planning to strongly tax or ban it, pushing the supply curve to the right.

- Alternatively, a firm might want to hold onto a product if they believe its demand will rise in the future, allowing them to sell it at a higher price.

- If a competitor is withdrawing or the government is making changes in regulations for example, it could drive prices up, which would motivate companies to withhold their products until they can sell them at a better price, shifting the supply curve to the left.

Price of Related Goods

- Just as consumers have the choice of what alternative good to purchase when the price of one changes, producers have a choice as to what to produce.

Joint Supply

- When two or more goods are derived from the same product, so that it is not possible to produce more of one without producing more of the other.

- The second good is often called a by-product.

- An increase or decrease in supply of one good results in a similar increase or decrease in the joint good.

Competitive Supply

- When the production of two goods uses similar resources and processes. When a supplier produces more of one good it means producing less of the other.

Global Events and Crises

- Global events and crises can cause disturbances in supplies.

- Namely wars and extreme weather events can cause decreases in supply by interrupting supply chains.

Number of Sellers

- As a market is the sum of all the individual suppliers of a product, when the number of suppliers that offer the same good increases, the market supply also increases, shifting the supply curve of that good to the right.

The Law of Diminishing Returns

- Eventually there is a point where suppliers don't want to supply a product due to the height of the price.

- This is because the costs of supplying the product eventually equal or outweigh the profits from supplying the product.

- Often producers have a choice as to what they are going to produce (similar products).

- The price increase in one product will increase the supply of the product but decrease the supply of the similar product.

Marginal Costs

- As you increase supply, the cost per product increases as additional supply will be less and less efficient.

- Marginal costs are defined as the increase in quantity supplied compared to the total cost of production.

- It can be interpreted as the opportunity cost of other products that producer could produce instead of an existing product.

Examples

- For example if you are producing pizza, having only one person in the kitchen would make pizza production very slow, resulting in a low supply.

- Adding one more worker to the kitchen could more than double the supply, with two people working together. The increase in supply will likely be worth the second worker's salary.

- However, the more workers you have in the kitchen, the more it costs to pay all the workers, but the less extra pizza they will be able to produce, due to getting into each other's way and not being able to coordinate as well.

- With higher prices, suppliers can face the marginal costs of increasing supply.

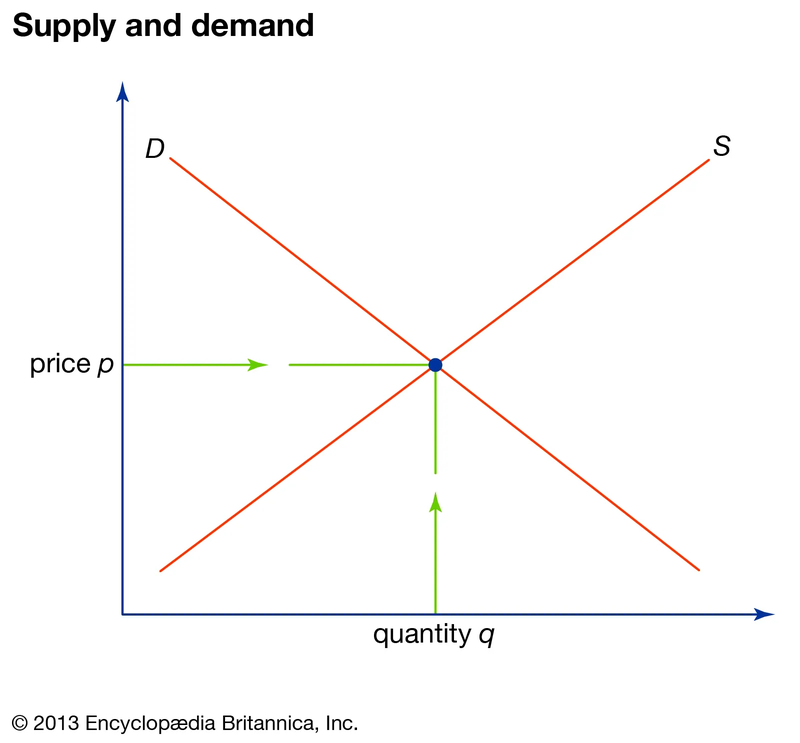

Demand and Supply

- Are demand graphs already giving you a headache? Well you're in for a treat as supply curves can also be graphed in tandem with a demand curve!

- Quantity (not quantity demanded or quantity supplied, just quantity!) is plotted as the x-axis and price as the y-axis.

- In a supply and demand curve, the two curves will take the form of two intersecting lines, looking like a cross.

- The two curves are independent from each other for the most part, however, special attention is required at the point which the two curves meet, which is called the market equilibrium.

Market Equilibrium

- Market equilibrium is the point on the graph where the supply and demand curves intersect.

- If the price of a good is at the market equilibrium, then that means that all the goods being produced are being exhausted by the market.

- There is no excess or shortage of supply.

Excess Supply

- When price is increased beyond the equilibrium point, the supply increases, but demand decreases. This means that there is more quantity supplied than there is quantity demanded.

- This leads to excess supply, which means the firm will eventually have to reduce their price back to the equilibrium as they lose money from the production costs of the excess goods they cannot sell.

Shortage

- A shortage is the opposite of excess supply.

- It occurs when the price is reduced to less than the equilibrium. Supply decreases, but demand increases.

- Eventually firms will increase their price back to the equilibrium as otherwise they are missing out on the possibility to sell for a higher price.

Sources