Classical Economists

- Classical economics is defined by a focus on studying supply instead of demand.

- Classical economists believe that supply will create its own demand.

- Free markets are also a key feature of classical economics, with economists such as Adam Smith saying that phenomena such as the "invisible hand" will lead to people acting in self interest to have a benefit for the greater good.

Adam Smith

- Adam Smith was a Scottish social philosopher that is often called "The Father of Economics".

- He lived during the 18th century and is best known for his work The Nature and Causes of the Wealth of Nations, which is often shortened to the Wealth of Nations.

- In the Wealth of Nations, Adam Smith advocates for free trade between countries and the importance of the specialization which it allows.

- He also introduced vital economic concepts such as the "invisible hand".

- His works were the groundwork for classical economics.

Jean Baptiste Say

- Jean Baptiste Say was a classical French economist that lived during the late 18th and early 19th centuries.

- He is best known for the coining of "Say's Law", which states that supply creates its own demand.

- Say's law says that entrepreneurship and the supply of goods/services leads to profit, wages, income, and spending resulting in an overall increase in demand as consumers now have a greater ability to spend (the source of demand is production).

- Say's law is the foundation for the circular model of economics.

David Ricardo

- David Ricardo was a British economist and politician that lived during the late 18th and early 19th centuries.

- He is influential for his coining of comparative advantage.

- Comparative advantage is the ability of an economy to produce a good or service in a more efficient or economically competitive way than its peers.

- Economies with comparative advantages for a specific resource often trade with other countries, which have a harder time producing the same resource.

Neoclassical Economics

- Neoclassical economics, also nicknamed "The Marginal Revolution" led to the conception of new ideas and thinking methods.

- The theory of marginal utility and increased focus on demand are signature features of this school of thought.

- It was during the rise of neoclassical economics that economics became recognized as an actual science.

- Economic thought became more mathematical and scientific.

- This led to the more prominent use of models and graphs.

- The assumption that the producer and consumer are rational was also first introduced by neoclassical economists.

Important Neoclassical Economists

William Stanley Jevons

- William Stanley Jevons was an American economist from the 19th century.

- He is notable for the his contribution to the marginal revolution and introduction of concepts such as Jevons' Paradox.

- Jevons' Paradox states that gains in fuel efficiency, will increase the use of that fuel.

- This thought has gained more importance with recent efforts to reduce pollution.

Leon Walras

- Leon Walras was a 19th-20th century French economist, best known for his creation of the perfect competition theory.

- The perfect competition theory is a hypothetical situation where lowering prices, and therefore improving efficiency is the only way for firms to compete.

- Perfect competition is useful for many theoretical studies of economics.

Carl Menger

- Carl Menger was a 19th-20th century Austrian economist.

- He is most notable for focusing on values and aiding in the creation of the theory of marginal utility and the subjective theory of value.

Alfred Marshall

- Alfred Marshall was a 19th-20th century English economist.

- He is most notable for writing the book Principles of Economics.

- His book structured the ideas of supply and demand, marginal utility, and costs of production as a coherent whole.

Utility

- Utility is the most important concept of Neoclassical economics.

- It is he measure of the satisfaction derived from consuming a good or service.

- Marginal utility refers to the extra or additional utility derived from consuming one more unit of a good or service.

- Marginal utility reduces as more of a good or service is consumed.

Socialism

- Capitalism led to great prosperity, however, it also created income/wealth inequality and prioritization of profit above all including working conditions, fair wages, etc.

- Socialism was an alternative economic system to capitalism, that aims to solve the problems of capitalism; but has problems of its own.

Karl Marx

- Karl Marx was a 19th century German philosopher and economist notable for his idea of Socialism, which was a very controversial but popular economic political system.

- His most famous writing is the book Das Capital.

- Karl Marx founded by an alternative economic system known as the command system where the government strives to allocate resources equitably.

- This would develop into socialism.

Keynesian Revolution

- The Keynesian revolution was a school of economic thought led by American economist John M. Keynes.

- The Keynesian Revolution took place during the 20th century.

- The Keynesian revolution focused mainly on the General Theory of Employment, interest and money.

- Keynesian economics mainly states the importance of government intervention through Fiscal and Monetary policy to promote economic stability.

- During a recession the government should run a budget deficit and spend money to boost the economy.

- From 1970s stagflation occurred, which led to high unemployment and high inflation, especially in economies using Keynesian policies.

- This would cause Keynesian economics to lose a lot of popularity.

Monetarism

- Monetarism is an economic theory that focuses on macroeconomics and the effect of supply of money and central banking.

- Monetarism's main belief is that central banks should restrict the money supply to the same rate as national output.

- More money supply than output leads to inflation.

- Monetarism was formulated by American economist and statistician Milton Friedman.

- Monetarism was formulated to challenge Keynesian economics and to prevent the Staglfation of the 1970s from occurring again.

- High budget deficits, lower interest rates, the oil embargo and the collapse of managed currency rates contributed to stagflation.

- Monetarists believe the main determinant of economic grwoth is the total amount of money in the economy and so their focus was mainly on monetary policy and money supply.

- Monetarists state that money supply should grow at the same pace as output and that governments should not try to manage demand.

21st Century

- Economics in the 21st century has changed in many ways, listed below.

- Increased collaboration among other academic disciplines, mainly psychology.

- Previously, economists have always assumed that producers and consumers act rationally. This means that they know the utility and cost of the product relative to others, and will always act in a logical and selfish way (for consumers buying the cheapest products with most utility, for firms maximizing profit).

- However, in reality, people rarely act rationally, and there are numerous factors that influence their decisions.

- A growing interest in behavioral economics to understand why and how economic agents make decisions.

- Increasing awareness about the relationship between economic activity and the environment.

- Increasing awareness about the relationship between economic activity and society.

- Increased focus on shifting to a circular economic model - an economic model where waste or pollution are phased out and materials are reused in production.

- There is now an urgent need to switch from our current linear economy to a circular economy.

Linear Economy

- Harvest natural resources from Earth.

- Produce from resources.

- Throw away products.

- Linear economies can only exist for a limited time, as the environment of the Earth increasingly worsens.

Circular Economy

- Harvest natural resources from Earth.

- Produce from resources.

- Reuse and recycle products to make new products.

- If efficient enough, circular economies can go on indefinitely.

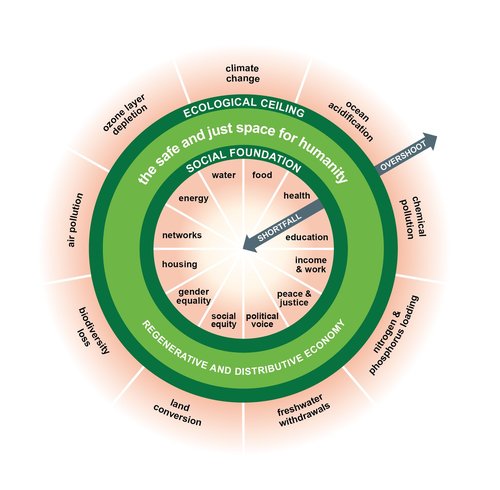

Doughnut Economy

- The doughnut economy is a visual model for sustainable development that was developed by British economist Kate Raworth.

- Producing enough to satiate social needs but not too much, otherwise would go through the economic ceiling.

Sources

https://commons.wikimedia.org/wiki/File:Doughnut_(economic_model).jpg

.jpg){kind=link}