Aggregate Supply

- Aggregate supply, similar to aggregate demand, is the macroeconomic equivalent of supply.

- It represents the total output that firms will produce and sell at a given average price level in a certain time period.

- It is split into long-run and short-run aggregate supply when using the neoclassical model.

Short-Run Aggregate Supply (SRAS)

- Total quantity of real output (real GDP) offered at different possible price levels in the short run.

- It slopes upward similar to a normal supply curve.

Shifters of SRAS

- The shifters of the SRAS curve generally occur due to the movement of the AD curve, but factors such as government policies can also cause a shift in the curve.

Costs and Availability of Resources

- A change in wage rates. An increase in wages causes increased production costs and shifts SRAS left, and vice versa.

- A change in the costs of raw materials. Increase in costs shifts SRAS to the left and a decrease shifts SRAS to the right.

- A change in the price of imports. An increase in import prices will decrease SRAS, depending on how many firms use imported materials in production. A decrease in import prices causes SRAS to shift right.

Government Intervention

- A change in government indirect taxes or subsidies. Subsidies increase SRAS and taxes decrease SRAS.

- Regulations can positively or negatively affect producers.

Supply Shocks

- An event that drastically alters supply such as a natural disaster or war.

- Usually results in a drastic leftward shift of the SRAS curve.

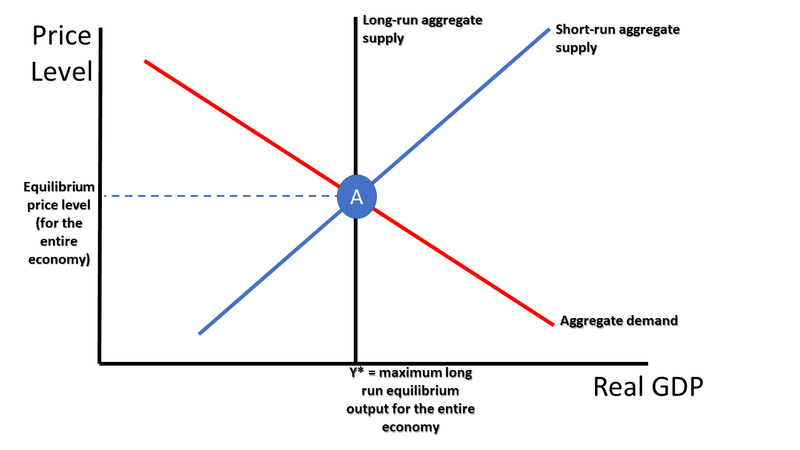

Long-Run Aggregate Supply (LRAS)

- Aggregate supply that is dependent upon the resources and technology in the economy, thus being dependent on the price level.

- It is a vertical line at the level of potential output.

- It can only be increased by improvements in the quantity and/or quality of factors of production as well as improved technology.

Graphs

- Short-Run Aggregate Supply Graph

- Similar to a normal supply graph in microeconomics.

- SRAS is an upward sloping curve.

- Price level in Y-axis and real GDP or equivalent in x-axis.

- LRAS is a vertical curve that cuts through the equilibrium.

Shifters of LRAS

- The shifters of LRAS are similar to the shifters of a PPC curve, as both represent the possible economic output of a nation.

- Change in quality or quantities of factors of production

- Technological improvements

- Increase in efficiency

- Changes in institution

Factors That Influence the Quality/Quantity of Factors of Production

- The factors of production are land, labor and capital and entrepreneurship.

Land

Increase in Quantity

- Land reclamation

- Increased access to supply of resources

- Discovery of new resources

Increase in Quality

- Technological advancements that allow for increased access to resources or the discovery of new resources.

- Fertilizers

- Irrigation

Labor + Entrepreneurship

Increase in Quantity

- Increase in birth rate

- Immigration

- Decrease in the natural rate of unemployment

Increase in Quality

- Education

- Training

- Re-training

- Apprenticeship programs

Capital

Increase in Quantity

- Investment

Increase in Quality

- Technological advancements that contribute to more efficient capital

- Research and development

Natural Rate of Unemployment

- The rate of unemployment that occurs when the economy is producing at its potential output or full employment level of output (Yf).

- Natural unemployment exists because there is still some unemployment at the full employment.

- Some people might be switching jobs, or be in training for example.

SRAS Non-Price Determinants

Neoclassical Model of Aggregate Supply

- Neoclassical economics was founded by Milton Friedman in the 1870s.

- General equilibrium approach is based on the school of neo-classical economics.

- Assumes prices are always flexible in the long-run.

- This diagram didn't do well at prediction as prices and wages tend to be less flexible.

- Enforces the idea that the market will fix it self and return to equilibrum (full employment).

- In the neoclassical model, the supply curve will move in response to changes so that LRAS is always cutting through the equilibrium.

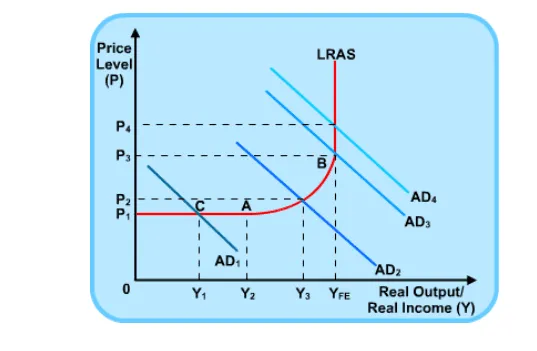

Keynesian Model of Aggregate Supply

- Founded by John Manyard Keynes in the 1920s/30s.

- The Keynesian model was a response to the neo-classical models which couldn't fix the great depression.

- States that wages are "sticky" and are slow to change due to labour laws, contracts, salaries, etc.

- Argues that the economy gets stuck in a short-run position.

Only one aggregate supply curve, no distinction between LRAS and SRAS.

Keynesian Aggregate Supply Graph

- Capacity: Maximum level of output possible.

- The Keynesian model has 3 phases.

- The Keynesian model has one AS curve that starts horizontally then curves vertically.

Horizontal Section

- A fair amount of spare capacity. Room to increase GDP without price level going up.

Upwards Sloping Section

- The graph starts to curve upwards as it transitions to the vertical section from the horizontal section.

- Still some spare capacity, yet competition for scarce resources begin.

Vertical Section

- Almost a fully vertical curve.

- Little to no spare capacity. Full employment reached.

- Price increases a lot compared to minor changes in real GDP.

Inflationary and Deflationary Gaps

Recessionary/Deflationary Gap

- When the equilibrium level of real output is less than the potential output as a result of a decrease in AD.

- The gap is the difference between the new aggregate demand curve and the aggregate demand curve at full employment.

- The deflationary gap is temporary.

- The deflationary gap can be seen on a business cycle graph as the difference between actual output and potential output.

Inflationary Gap

- When the equilibrium level of real output exceeds the potential output as a result of an increase in AD.

- The gap is the difference between the new aggregate demand curve and the aggregate demand curve at full employment.

- The inflationary gap is temporary.

- The inflationary gap can be seen on a business cycle graph as the difference between actual output and potential output.

Stagflation and Growth

- Stagflation is a decrease in real GDP and an increase in unemployment rates simultaneously.

- Stagflation is extremely undesirable for an economy.

- Typical growth may also occur in the short run.

Disequilibrium in Aggregate Supply

Short Run Equilibrium

- There can be inflationary or recessionary gaps, but will eventually return to equilibrium.

Long Run Equilibrium

- In the short run, inflationary and recessionary gaps exist.

- However, in the long run, the equilibrium point must return to the LRAS (full employment).

Connection to Business Cycle

- The deflationary gap can be seen on a business cycle graph as the difference between actual output and potential output.

- Graphically, it is the vertical difference between the growth-trend line and the fluctuating actual output line.

- Long term aggregate supply changes as the general growth trend (potential output) increases over time.

- As the economy grows over time, the LRAS curve gradually shifts to the left.

Connection to the PPC Curve

- Points on the PPC curve can show inflationary and deflationary gaps as well.

- A point on the PPC curve is when there is equilibrium and SRAS = LRAS = AD at the GDP at full employment.

- Points below the PPC curve represent a deflationary gap as resources are not at full employment.

- Points above the PPC curve could represent an inflationary gap as resources are beyond full inflation.

- There is a slight discrepancy with this connection, as in a PPC diagram points beyond the curve are said to be impossible.

- The Keynesian model does not share this discrepancy as when there is an inflationary gap AS is perfectly inelastic and therefore output cannot increase alongside increases in demand.

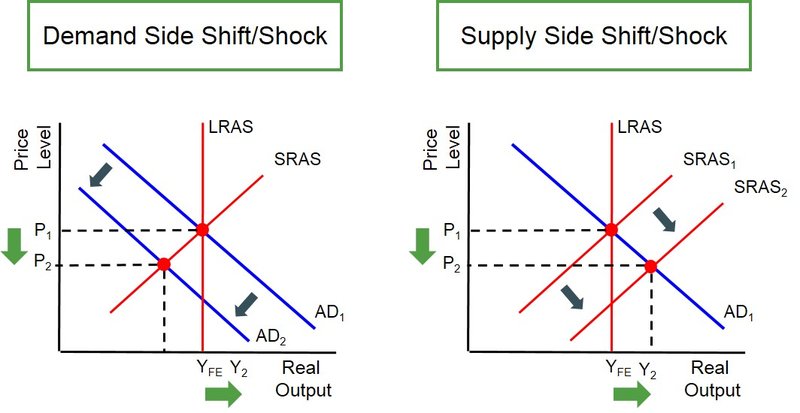

Long-Run Equilibrium Adjustments

AD Decrease

- A decrease in AD results in a decrease in price level across the economy.

- This results in the cost of inputs (such as wages) lowering, allowing companies to hire more workers and therefore increasing SRAS.

- The new price level at the equilibrium is now lower than the original.

AD Increase

- An increase in AD results in an increase in the aggregate price level.

- This results in increased production costs (wages, materials, etc.), leading to a reduction in SRAS.

- The new price level equilibrium is now higher than the original.

Neoclassical vs Keynesian Aggregate Supply.

Neoclassical

Equilibrium

- A market in disequilibrium will always correct naturally.

Wages

- Wages are flexible and can easily change.

Intervention

- Government intervention is not needed.

Keynesian

Equilibrium

- A market in disequilibrium may stay in disequilibrium for extended periods

Wages

- Wages are {"sticky" and do not change easily.

Intervention

- During a recession, the government must increase government spending to correct the recession, even if it must borrow funds.

“But this long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is long past the ocean is flat again.”

J.M. Keynes, 1936.

Sources

https://studymind.co.uk/notes/aggregate-supply-a-level-economics/

https://corporatefinanceinstitute.com/resources/economics/inflationary-gap/

https://www.nuffield.ox.ac.uk/Users/Cameron/lmh/pdf/m8-04.pdf